Rising Interest Rates Impact Both Buyers and Sellers

As we head into the holiday season, inflation remains stubbornly high, whether you’re shopping for food, clothes, or a home, it seems like everything is more expensive these days. The consumer price index, a broad-based measure of goods and services costs increased 0.4% for the month and 7.7% from a year ago, according to the US Bureau of Labor Statistics data published on November 10th. To cool things down, the Federal Reserve has taken aggressive action and has been steadily increasing the federal funds rate, from 0% less than a year ago to almost 4% today. This action directly affects the cost of borrowing for banks, as they lend and borrow from each other to help maintain required reserve levels. Although mortgage rates and the federal funds rate aren’t directly correlated, they typically move in the same direction and this has resulted in a rise in mortgage interest rates, the average 30-year fixed rate mortgage rate is now 6.58%, which is up 3.5 points vs. last year.

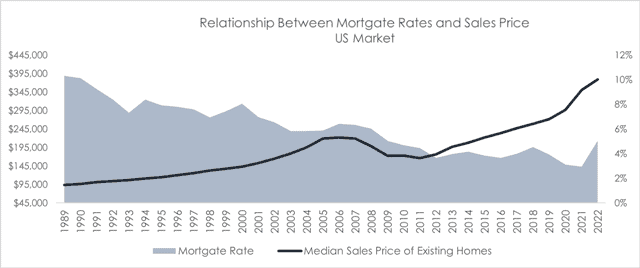

HISTORICAL PERSPECTIVE

While it’s true that rising mortgage rates will increase the cost of borrowing, I think it’s important for us to consider where we are today vs. where we have been in the past; this provides a bit of context to help keep the current market environment in perspective. First, it’s important to note that the current interest rate of 6.58%, while up +3.5 points to last year is down vs. this year’s high of 7.08%, this would suggest that the upward trend may be slowing. Second, when you look back in time, you can see that we have been at historical lows the past six years, averaging around 3.7%, which is well below a high of 10% back in 1989/90. If you go back even further, we were in the mid-teens for mortgage rates in the early 80’s. Adding an additional layer, we also included the median sales price of homes, you can see there tends to be an inverse relationship between the two, when interest rates are low, home prices increase. In 2021 we experienced an unprecedented +18% increase year over year in home prices, fueled by low interest rates and a strong recovery from the Covid-19 pandemic, this also contributed to higher levels of inflation. Relationship Between Mortgage Rates and Sales Price US Market Mortgage Rate Median Sales Price of Existing Homes

IMPACT TO BUYERS

Using history as a guide, if interest rates remain elevated, I believe we can expect to see home prices pull back from their highs. Home buyers looking to purchase a home with a mortgage will end up qualifying for a lower loan amount. Lenders will extend credit based on several factors but will consider how much of a down payment the borrower is able to make and what monthly payment you can afford based on your debt-to-income (DTI) ratio. Since more of your monthly payment will be going to interest, you will have less purchasing power. This will likely have the greatest impact for first-time homebuyers since they won’t have the equity from another home sale to support a higher down payment. Buyers may also have a hard time finding homes in their price range, while a pull back in pricing is likely to occur at some point, it may not occur immediately or as dramatically in relation to interest rates. This is due to several factors but is mostly an issue of supply – now, in the US and in Lincoln, there is not enough supply to keep up with demand, which could mean that prices remain elevated. Higher rates mean higher mortgage payments, this means that you will need to budget higher housing costs.

IMPACT TO SELLERS

Considering the significant increase in home values over the last 5 years, averaging +9% on an annualized basis, you will likely have accumulated significant equity in your home, depending on how long you have owned it. However, with rising rates, there are a few things to consider:

There may be less buyers in the market, according to Redfin, nearly 1/3 of US homes were purchased with cash in July of 2022, suggesting that the largest pool of buyers would be beholden to mortgages and impacted by higher rates. Higher home prices means that if you sell your home, you too will be in the market for a new place and will likely pay a higher price.

While difficult to predict, your home may not sell for as much, it’s hard to determine exactly what impact rates will have and how supply will affect this equation, but at some point, it’s likely that the rapid rise in sales prices will stabilize or fall a bit. The good news is that you are still likely to have build up equity in your home due to the sustained rise in prices over the last several years.

WHAT CAN BUYERS DO

Rising interest rates are certainly not ideal, but it doesn’t mean that you can’t find your perfect home. There are many factors that need to be considered, including your personal financial situation and your willingness and ability to pay slightly more for that mortgage payment each month. The good news is that you will now be in a market with less competition and will likely have more power in negotiating with sellers.

Prior to applying for a mortgage, make sure your finances are in good order. Pay down debt, this directly impacts your Debt-to-Income ratio (DTI) that lenders look for.

- Improve your credit score – this has a big impact on the rate your lender will offer, higher credit scores typically mean you will get the best rates available.

- Make sure you have a solid down payment, this will impact how much a lender is willing and able to offer and will impact the rate they offer as well.

- Find a great realtor to help navigate this challenging and dynamic real estate market. A good agent will help you find property within your budget and will be able to assess trends in the market to ensure you negotiate a fair price.

THE BOTTOM LINE

Despite a rise in mortgage interest rates, For buyers, we've seen a rise in the days on market, which is the time it takes from the time a property is listed until it is sold, this has led to more properties being sold below list price and creates an opportunity to buy a home with less competition and greater value. In fact, October had a sale price to list price ratio of ~91%, which is down from January of 2022 at 103%. For sellers, home price appreciation is significant in Lincoln, which makes it an advantageous time to sell your home. For context, the average home price in Lincoln is up 83% in October vs. January of 2020.

If you’re interested in buying or selling your home in the Lincoln area, please give me a call, I'm happy to help you with any and all your real estate needs.

Nick Dufour

Realtor – Alpine Lakes Real Estate

Lincoln, New Hampshire

78 Main Street, Lincoln, NH 03251

O: 603.745.3601